Overview

As we reflect on the first quarter of 2025—and the early days of April—it’s clear that markets have been tested by intense volatility. Much of this has been driven by the Trump administration’s sweeping trade and tariff actions, which represent not only a break from convention but also, according to many experts, a potentially risky structural shift with long-term consequences.

It’s not just the policies themselves but the manner in which they’ve been rolled out—bypassing diplomatic norms and traditional processes—that has eroded trust among global leaders and amplified uncertainty. Markets dislike ambiguity, and this level of unpredictability has prompted sharp reactions.

In a partial retreat, the administration announced a 90-day pause on certain tariffs for most countries—though the broader 10% blanket tariff remains in effect. While this temporary relief is encouraging, much depends on how upcoming bilateral negotiations unfold. There’s hope this pause could pave the way for de-escalation, but uncertainty persists.

A central issue remains the escalating trade conflict between the United States and China—the world’s two largest economies—an economic standoff with broad global implications.

There’s broad agreement that aspects of the U.S.–China trade relationship need to be reevaluated. However, many question whether the administration’s confrontational approach is the most effective or sustainable path forward.

At the heart of the administration’s strategy is the belief that trade deficits are inherently harmful and that aggressive tariffs are the necessary remedy. Yet most economists, central bankers, and business leaders argue that tariffs function as taxes—raising costs for consumers and disrupting global supply chains. Many see this approach as introducing significant economic risk.

In this newsletter, we review key market developments from Q1 and early April and provide historical context to help frame today’s environment.

Market Returns

Index Returns

YTD*

1yr

3yr

5yr

S&P 500 Total Return

-8.47%

3.47%

7.13%

15.32%

S&P 500 ESG Index Total Return

-9.42%

1.84%

6.92%

15.84%

Russell 2000 Total Return

-17.58%

-8.47%

-1.36%

9.44%

MSCI ACWI Ex USA Total Return

0.07%

1.94%

3.79%

9.47%

Bloomberg US Aggregate

1.28%

5.39%

0.73%

-0.86%

Navigating turbulent markets requires discipline and a long-term perspective. In a recent commentary featured in Clearnomics, James Liu and Lindsey Bell speak to the tension investors face between reacting to short-term volatility and staying focused on enduring goals. They cite a fitting quote from F. Scott Fitzgerald:

“The test of a first-rate intelligence is the ability to hold two opposed ideas in the mind simultaneously and still retain the ability to function.”

This idea—balancing opposing forces—is central to successful investing. As Liu and Bell point out, maintaining perspective during periods of uncertainty can help investors stay grounded in their broader financial objectives.

While the near-term outlook is clouded by geopolitical and economic challenges, our commitment is to help guide you through the noise. If you’re feeling unsettled or want to revisit your financial plan, we encourage you to connect with your advisor.

Investment & Economic Highlights

The State of the Economy

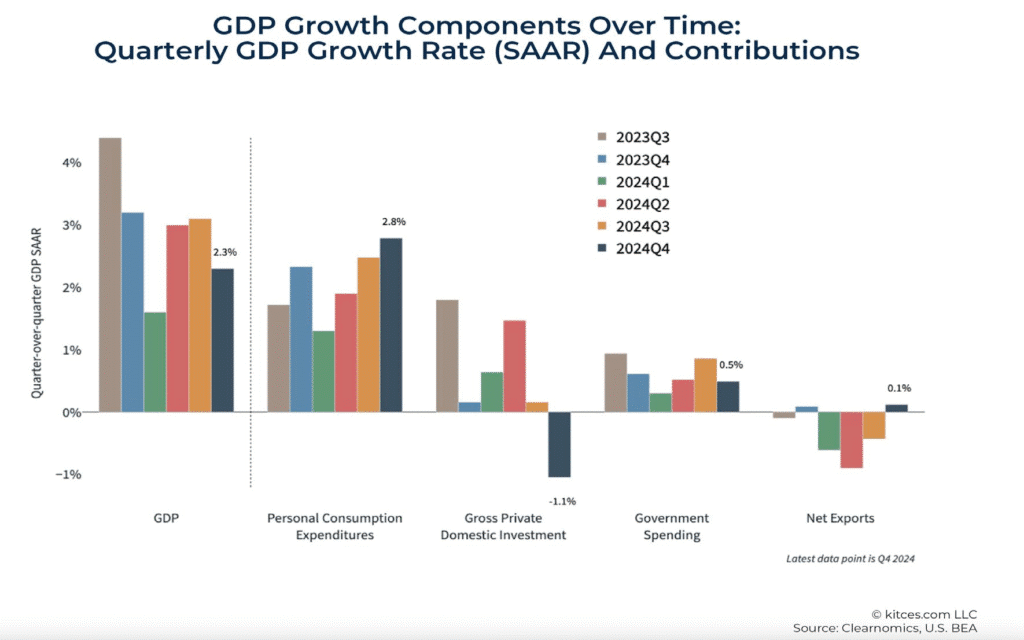

GDP: As evidenced by the chart below, US GDP (Gross Domestic Product) has been strong for the last six quarters, averaging roughly 3% but trending downward. The chart also shows how the final quarter of last year was buoyed by particularly strong consumer spending.

First quarter 2025 GDP is predicted by the Atlanta branch of the Federal Reserve to come in at 1.8%,excluding net imports. However, due to looming tariffs and growing political and economicuncertainty, net imports in the first quarter are believed to have skyrocketed to the point that overallGDP is projected to contract at a 2% to 3% annualized rate during the quarter. Over 40% of theseimports are estimated to be attributable to gold purchases, which contributed to gold prices soaringby more than 15% in the last three months. It should be noted, however, many economists (asindicated by a recent CNBC survey) remain more optimistic about first-quarter GDP and still expectmodest overall growth.

Consumer Sentiment: As surveyed monthly by the Conference Board, consumer sentiment droppedsharply in both February and March. Their forward looking “expectations index” also droppedsignificantly, reaching to its lowest point in 12 years. Consumer confidence is often considered a“contra-indicator” with the stock market, meaning that when pessimism reaches its peak, this isusually when the market turns around. It is not a contra-indicator for the economy, however, andlower consumer spending is expected to slow growth.

Investment & Economic Highlights

Interest Rates, Inflation, and Employment: From early 2022 through mid-2023, the Fed raised interest rates by 5.25% to combat inflation. Rates peaked at 9.3% during that time frame as measured by the U.S. Consumer Price Index (CPI). Last year, inflation slowed to the 3% to 4% range, and the Fed was able to start cutting rates. From September through year-end, rates were lowered by a total of 1%.

Core inflation (excluding energy and food prices) has also declined, but at a stubbornly slow pace. Itdropped from an annual rate of 3.8% a year ago and 3.2% last December to 3.1% in February (thelatest data available). While inflation has been gradually declining, it remains well above the Fed’s 2%target. This is another reason why the Fed has been reticent to cut rates further so far this year.Further rate cuts are expected, but inflationary pressure from higher tariffs has given the Fed pause.

The Fed’s higher-for-longer interest rate strategy has cooled the labor market, but not by much. Unemployment in the U.S. rose from 3.9% a year ago to 4.2% at quarter end.

The State of Investing

First Quarter 2025 Market Review: Investment returns during the first quarter were distinctly mixed.U.S. stocks performed poorly, with the S&P 500 large cap index down 4.3% and the Russell 2000 smallcap index down 9.2%. These losses, however, were offset to some degree by gains in both bonds andinternational stocks. International developed markets indices outperformed the S&P 500 by close toten full percentage points (up 5.7% vs down 4.3%). As a result, well-diversified portfolios typically hadmuch smaller losses and potentially even gains in the first quarter, despite the sell-off in the U.S.equity market.

Economic and Market Update as of April 11th : On April 2nd, the Trump administration introduced anambitious platform of global tariffs. This triggered dramatic stock market volatility. During the nexttwo days, the S&P 500 lost 9.6%, the Russell 2000 small cap index dropped 9.2%, and the ACWIinternational index (ex US) dropped 3.9%. On April 9 th , the administration paused a majority of tariffsfor 90 days for most countries except China. The S&P 500 advanced 9.5% on this news beforeretreating 4% on April 10th . Although the market has recovered some losses, most major indexesclosed below their original levels on April 2nd, when the tariffs were announced.

While it appears that volatility won’t go away anytime soon, the silver lining to this downturn is that

the S&P 500 is now valued more closely to historical norms but still above its 30-year average.

Recovering From Down Markets

Last month marked the five-year anniversary of the COVID bear market bottom in 2020. In case you were wondering, the S&P’s return since that COVID-low has been an annualized return of more than 17% per year. While volatile markets almost always spark fear in the minds of investors (and right now is no different), it’s worth noting that ‘staying the course’ has generally been a very good strategy.

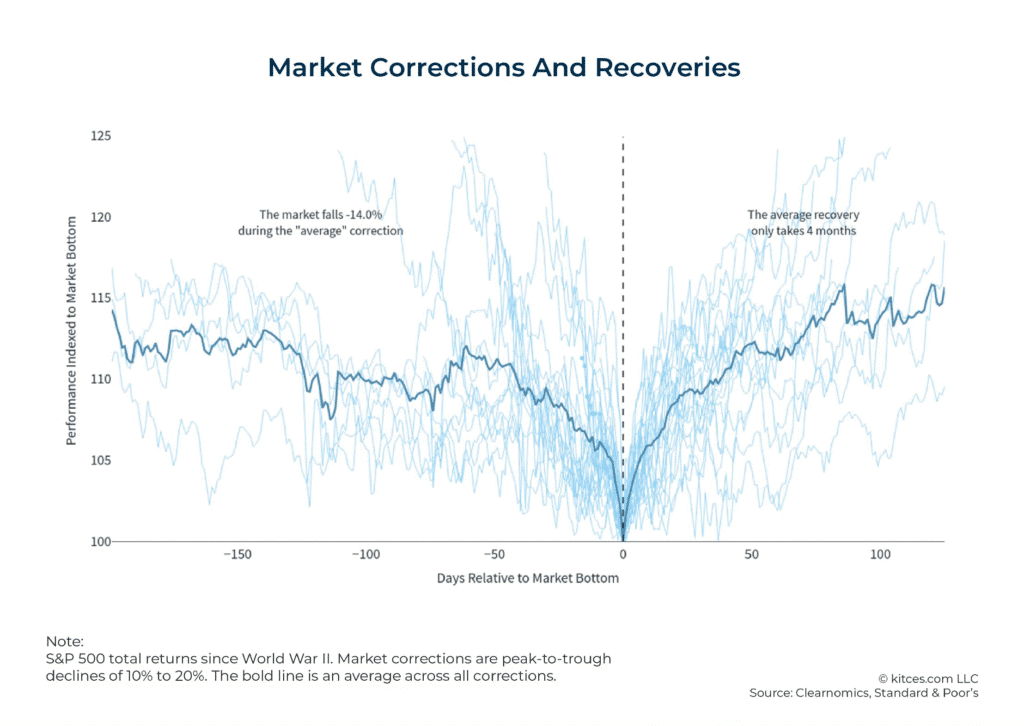

Clearnomics puts it this way: While past performance cannot guarantee future results, historydemonstrates that markets often recover from corrections when investors least expect it. Despite theseperiodic declines, the long-term trajectory of the market has historically been upward. During the 2020pandemic-related correction, the market recovered its losses in just five months, while the 2022correction took about a year…What makes these recovery periods particularly challenging for investorsis their unexpected nature. Market rebounds often begin during periods of maximum pessimism, whennegative headlines are still dominant and sentiment remains poor. This timing mismatch frequentlyleads investors to exit positions when markets are most attractively valued.

The chart below shows that since World War II, the average time for the market to recover from a 10% and 20% correction is about four months (deeper drops typically take longer). But as always, past performance can’t be relied upon as being indicative of future returns.

The current downturn in the market is largely a self-inflicted one. It appears to have been caused by the dramatic introduction of global tariffs, a policy which could potentially be reversed or modified at any time. In addition, the resulting global trade war and market downturn are likely to lead to the Fed cutting interest rates, which is typically helpful for stock market values. While we can’t know if such policy changes are coming, they certainly seem possible.

Two Reasons for Optimism

Global GDP is Expected To Rise Significantly Over The Decades Ahead: It’s easy to get caught up inthe day-to-day news stories and become pessimistic about nearly everything in life. But, as weroutinely strive to remind you, the world is improving nearly everywhere around us, even if the newsmakes it seem like it’s not. As one example of this progress, many of the world’s largest economies areexpected to continue expanding dramatically over the next few decades. And when the world getsricher (along with healthier and safer, generally speaking), it seems reasonable to assume thecompanies that provide goods and services to those consumers should, hopefully, thrive as well.(Source: Goldman Sachs)

Zero Carbon Power Is On The Rise: While climate change seems to be a highly politicized issue, zero-carbon power is an unquestionable positive for humanity’s future. We’re now seeing nuclear powermaking a comeback, with more than forty countries putting projects in place to establish or expandtheir nuclear capacity. Thanks in part to the cost of solar panels dropping by nearly 90% over the lastdecade, the combination of wind and solar generated more power in the U.S. than the coal industryfor the first time ever in 2024. (Source: Nuclear: Atlantic Council; Wind & Solar: Not Boring)

Sharing Resources

Our team is constantly reading and digesting interesting information. This section highlights a few items that piqued our curiosity this quarter.

The secret to living an unforgettable life every year – This video is only 2:38, but presents some interesting ideas around living a rich life. In times when things feel out of our control, reassessing personal goals and philosophies can be a fulfilling thing to turn mental energy towards.

Something that has historically made our economy and markets thrive is private companies’ ability to innovate over time, during good times and bad. Check out this fascinating look into Costco and their choice to bring their private label to the forefront.

CCM Spotlight

We might be biased, but we have the best staff at CCM. We wanted to dedicate some space here to let our staff shine and help you get to know us all a little better.

This month we are spotlighting Vince. As of this March, Vince celebrated his five-year anniversary with CCM. He enjoys simplifying financial worries into clear, actionable plans for his clients.

Thank you for continuing to trust in our team. We appreciate the opportunity to play a part in your financial future.

Most sincerely,

Your CCM team

Born and raised in Colorado, Vince relocated to sunny Florida in late 2023 with his girlfriend, Allison, where they spend their free time golfing, relaxing at the beach, and fishing. He flies back to Colorado quarterly to meet clients in person, reconnect with family, and visit with the CCM team. Fun fact: Vince holds dual citizenship with France and plans to brush up on his French before a trip this fall!

- If you would like to schedule time with us, please reach out to your advisor and we will happily arrange it.

- If you think of anyone who may benefit from the work we do, we would be delighted to talk to them to see how we might be able to help.

Join our newsletter

Our annual impact report provides an overview of our work, the markets, etc…