Key Takeaways:

- A retirement portfolio works best when each dollar has a clear job: liquidity, income, or long-term growth.

- Balancing these three roles can help support spending needs while reducing unnecessary investment risk.

- A thoughtful portfolio structure can improve flexibility through changing markets and retirement stages.

Retirement changes the job of a portfolio.

During the working years, the portfolio is often something being built for the future. Contributions go in. Paychecks arrive. Market downturns may be uncomfortable, but they can feel somewhat removed from daily life because income is still coming from work.

In retirement, the flow changes.

The same portfolio that once represented the future may now help fund the present. That shift is not just financial. It is emotional.

For some people, retirement feels like an on/off switch. Work stops, the paycheck ends, and a new chapter begins. For others, it is more like a dimmer switch. They slow down gradually, consult for a while, keep some earned income, or move into a different rhythm of work and life over time.

Either way, there is often a moment when retirement starts to feel real.

We may have talked with clients about the plan many times before they retire. We may have reviewed Social Security, portfolio withdrawals, taxes, cash reserves, and the life they want to live. The plan may make complete sense on paper.

But understanding the plan is not the same as living it.

A person can be well prepared, excited to retire, and fully ready for what comes next — and still wake up one day with a very practical question:

“So what is our strategy now?”

That question is not a sign that the plan was unclear. It is a sign that the experience has changed.

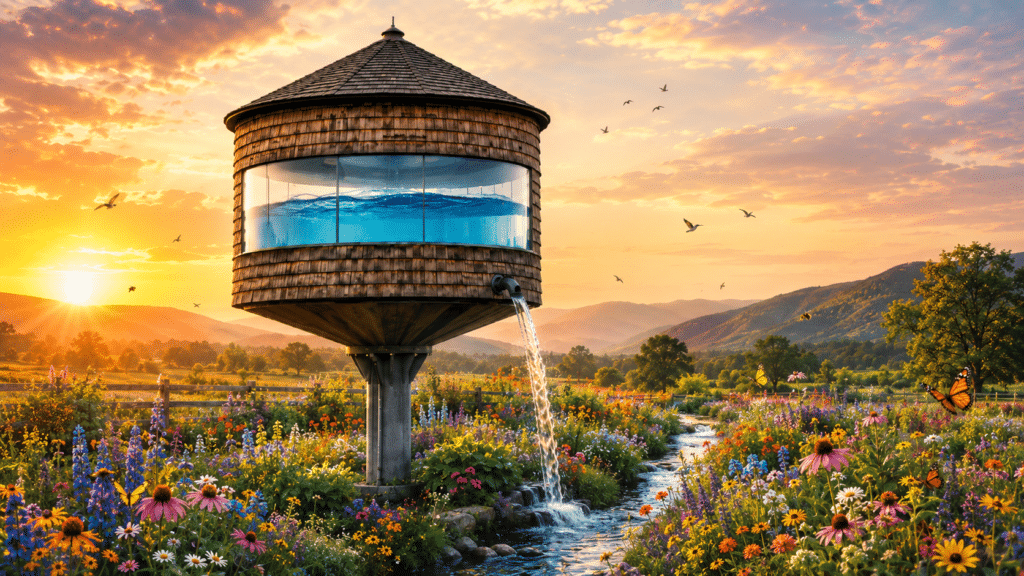

A helpful way to picture this is a water tower. During the working years, you are steadily filling it. The level may rise and fall with markets, savings, and life events, but the general direction is clear. In retirement, water begins flowing out. The tower may still be refilled through investment returns, income, or other resources, but it feels different when you begin drawing from what you have built.

That is why retirement portfolio planning is about more than choosing investments. It is about creating a structure that helps your portfolio support your life.

Table of Contents

- 1. A Retirement Portfolio Has Three Jobs

- 2. Job One: Liquidity for Breathing Room

- 3. Job Two: Income for Current Spending

- 4. Job Three: Growth for the Future

- 5. This Is Related to a Bucket Strategy, But It Does Not Have to Be Rigid

- 6. The Right Balance Depends on the Broader Plan

- 7. Confidence Comes From Structure, Not Certainty

- 8. Frequently Asked Questions

- 8.1. 1. What are the three jobs of a retirement portfolio?

- 8.2. 2. Why is liquidity important in retirement?

- 8.3. 3. What is retirement income planning?

- 8.4. 4. What is a total return approach to retirement income?

- 8.5. 5. Is this the same as a retirement bucket strategy?

- 8.6. 6. Why does growth still matter in retirement?

- 8.7. 7. What is a retirement withdrawal strategy?

A Retirement Portfolio Has Three Jobs

Most retirees are not trying to solve one problem.

They need accessible money for near-term needs. They need a way to fund regular spending. They also need part of the portfolio to remain invested for a future that may last 20, 30, or more years.

Those needs can pull in different directions.

Too much cash can feel safe, but may make it harder for the portfolio to keep pace with inflation. Too much focus on income can lead to a portfolio that is overly dependent on yield. Too much growth can create more volatility than a person is comfortable living with once withdrawals have begun.

A thoughtful retirement portfolio does not ask one part of the money to do every job. It gives different parts of the portfolio different roles.

The three core jobs are:

Liquidity for breathing room.

Income for current spending.

Growth for the future.

Job One: Liquidity for Breathing Room

Liquidity comes first because real life does not move in a straight line.

Retirees may need cash for monthly spending, taxes, travel, home repairs, health care, family support, charitable giving, or larger purchases that do not fit neatly into a monthly budget. Some expenses are predictable. Others arrive in waves.

Liquidity gives the plan breathing room.

It can also reduce the pressure to sell long-term investments at the wrong time. A portfolio may be well designed for the long run, but it can still be difficult to live with if there is no accessible source of cash when markets are down or life becomes more expensive than expected.

Liquidity is not about keeping money idle for no reason. It is about having enough flexibility to avoid being forced into poor decisions.

The right amount is personal. It depends on spending needs, income sources, risk tolerance, taxes, account types, and comfort level. Too little liquidity can create stress. Too much liquidity can hold back long-term growth.

A good retirement plan should help answer a simple question: if something comes up, where does the money come from?

Job Two: Income for Current Spending

Once liquidity is in place, the next question is income.

Retirement income planning is not just about dividends, interest, or bond yields. Those can all play a role, but they are not the whole picture.

In many cases, it is more helpful to think in terms of total return. A portfolio can support spending through a combination of interest, dividends, distributions, and disciplined withdrawals from appreciation over time. That means being intentional about when and how investments are sold, so the income plan is connected to the overall investment strategy rather than forcing the portfolio to produce all spending needs through yield alone.

Retirement income often comes from several sources: Social Security, pensions, portfolio withdrawals, required distributions, interest, dividends, real estate, business income, or part-time work.

The practical question is straightforward: how will the lifestyle be funded?

That answer should be coordinated with the broader plan. Which accounts should be used first? How should taxes be managed? How much should come from cash reserves, taxable accounts, retirement accounts, or other sources? How do planned withdrawals fit with the investment allocation?

This is where retirement can feel different from the working years. A person may have spent decades saving and investing. Now the portfolio has to become part of the paycheck.

That shift can be emotional even when the math works.

A good income plan helps make the process understandable. It shows where spending money is expected to come from, how the plan may adjust over time, and how regular spending fits alongside larger, less predictable needs.

The purpose is not simply to produce income. It is to support the life you want to live now while keeping the future in view.

Job Three: Growth for the Future

Growth still matters in retirement.

That can sound counterintuitive. Many people assume retirement means becoming much more conservative. Sometimes a portfolio should become more conservative. But moving too far in that direction too soon can create a different risk: the risk that the portfolio is not well positioned for a long retirement.

Retirement can last many years. Inflation, health care costs, housing, family needs, charitable goals, and longevity can all place pressure on a portfolio over time.

Long-term growth is not about chasing returns. It is about keeping part of the portfolio invested for future needs while making sure the overall structure still supports current spending and near-term flexibility.

The right balance is personal. A retiree with a pension that covers most living expenses may need a different portfolio than someone relying heavily on portfolio withdrawals. A family with large charitable goals may need a different structure than one focused primarily on lifetime spending. Some people value stability and simplicity. Others are comfortable with more fluctuation if it supports the long-term plan.

The investment strategy should reflect the real purpose of the money.

This Is Related to a Bucket Strategy, But It Does Not Have to Be Rigid

Some people describe this as a retirement bucket strategy.

That can be a useful way to think about it. Some money is meant to be available soon. Some provides flexibility. Some remains invested for later years.

But the structure does not have to be rigid or formulaic. Not every person needs the same number of buckets, the same time periods, or the same allocation. What matters is that the portfolio is organized in a way that makes sense for the person living with it.

A clear structure can help retirees avoid feeling like every market move requires an immediate decision. If near-term needs are covered, and the income plan is clear, it can be easier to let the long-term portion of the portfolio do its job.

That does not remove uncertainty. But it can make uncertainty easier to live with.

The Right Balance Depends on the Broader Plan

Two people with similar investment balances may need very different retirement portfolios.

One may have steady pension income. Another may depend more heavily on portfolio withdrawals. One may want to help children or grandchildren. Another may have significant charitable goals. One may be comfortable with market volatility. Another may need more stability to sleep well at night.

This is why retirement portfolio planning cannot be separated from retirement planning itself.

The portfolio is one of the main tools used to support the plan. It should be connected to spending, taxes, health care, estate planning, family priorities, charitable goals, and the client’s own sense of what they want retirement to feel like.

At Colorado Capital Management, we believe investment strategy should be grounded in the real purpose of the money. That means using diversification, cost awareness, tax awareness, risk management, and long-term discipline in service of the client’s broader life and planning goals.

The portfolio is not separate from the plan. It is part of how the plan becomes real.

Confidence Comes From Structure, Not Certainty

A thoughtful retirement portfolio plan does not make the future predictable.

No plan can know exactly when markets will be difficult, when a roof will need attention, when a family need will arise, or how long retirement will last. Spending may be higher in some years and lower in others. Priorities may change. Retirement itself may unfold differently than expected.

But structure helps.

It helps clarify what part of the portfolio is meant to support near-term needs, what part is expected to fund ongoing spending, and what part remains invested for the future. It can also make it easier to stay disciplined when markets are volatile or life becomes more complicated.

The purpose is not to predict every turn in the road.

The purpose is to give different parts of your wealth a job, so your portfolio can support both the life you want to live now and the future you are still planning for.

Frequently Asked Questions

1. What are the three jobs of a retirement portfolio?

A retirement portfolio often needs to provide liquidity for near-term needs, income for current spending, and long-term growth for the future. The right balance depends on the broader retirement plan.

2. Why is liquidity important in retirement?

Liquidity gives a retirement plan flexibility. It can help cover spending needs, taxes, unexpected expenses, and larger purchases without forcing the sale of long-term investments at an unfavorable time.

3. What is retirement income planning?

Retirement income planning is the process of determining how spending will be funded after work income stops or slows down. It may include Social Security, pensions, portfolio withdrawals, required distributions, interest, dividends, and other income sources.

4. What is a total return approach to retirement income?

A total return approach looks at the full return of the portfolio, including interest, dividends, distributions, and price appreciation. Rather than relying only on yield, withdrawals are coordinated with the investment strategy, tax plan, and spending needs, including thoughtful decisions about when and how to sell investments.

5. Is this the same as a retirement bucket strategy?

It is related, but it does not have to be a rigid bucket strategy. The broader idea is to match parts of the portfolio with the timing and purpose of future needs.

6. Why does growth still matter in retirement?

Growth can help a portfolio keep pace with inflation, health care costs, longevity, family needs, charitable goals, and other future priorities. Even in retirement, part of the portfolio may need to remain invested for the years ahead.

7. What is a retirement withdrawal strategy?

A retirement withdrawal strategy is a plan for how money will be taken from different accounts over time. It may consider spending needs, taxes, required distributions, market conditions, and the overall investment allocation.

Lee Strongwater is President and Senior Advisor at Colorado Capital Management, a Boulder-based, fee-only fiduciary wealth management firm. With more than 20 years of experience in financial planning and investment management, Lee helps individuals and families make thoughtful decisions about retirement, investing, tax-aware wealth strategies, and long-term financial planning.

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

- Lee Strongwater, WMS®

Editor’s Note: This blog post is for informational purposes only and does not constitute financial, legal, or tax advice. Readers are encouraged to consult with a qualified professional regarding their individual circumstances. Please refer to our firm’s website for full disclosures and important information: CCM Website Disclaimer